A loan shark is a person or body offering loans at extremely high interest rates. When we hear the term, we usually think about gangsters who lend money to people but enforce repayment through methods like blackmail and threats of violence. However, what you may not know is that while loan sharks are mostly seen as figures in the criminal underworld and organized, they’re not always seen as crooks linked to the mob, especially in the world of small time and salary lending. Historically, it wasn’t unusual for many moneylenders to skirt between legal and extralegal activity. In late 19th century America, the unprofitability and negative societal perception of small loans paved the way for a slew of lenders offering loans at profitable but at illegally high interest rates under a veneer of legality and preyed upon a borrower’s ignorance of the law. The 1920s and 1930s saw a rise of loan sharks who targeted high risk borrowers and small businesses either in dire straits or ill repute as well as enforced repayment through threats of violence. Sometimes these loan sharks were affiliated organized crime but they never had such monopoly. Today our non-standard lenders consist of subprime loans which led to a global financial crisis and payday lending which are both legal. But both are rather exploitative and prey upon those who can’t qualify for standard loans on mainstream sources. Yet, it’s the payday loans that generally don’t receive the attention they should since they’ve come under tremendous scrutiny as a predatory enterprise and must be stopped. Here I provide a small cheat sheet for explanation.

It’s likely you may see a lot of payday loan ads like this. A payday loan is a small unsecured loan that’s typically due on the borrower’s payday. However, they tend to have an reputation of high interest rates.

What is a payday loan?

A payday loan is a small short-term unsecured loan that’s typically due on the borrower’s payday. They usually range from $100-$1,500 and are often due 30 days or less. A payday loan relies on the consumer having previous payroll and employment records. In a payday loan, a borrower gives the lender access to their checking account or writes a check for the full balance that the lender has an option to deposit when the loan comes due. Other loan features can vary. Though payday loans are often structured to be paid off in one lump sum payment, interest only payments known as “renewals” or “rollovers” aren’t unusual. In some cases, payday loans may be structured so they’re repayable in installments over a longer period of time. Payday loans usually include a finance that may range from $10-$30 for every $100 borrowed or the check’s percentage value.

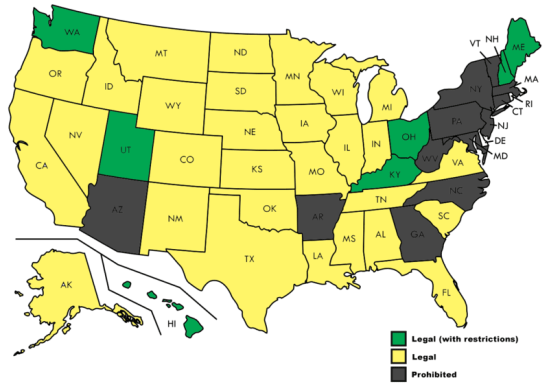

While payday loans are legal under federal law, state laws may vary. My home state of Pennsylvania is one of the states that prohibits them outright as you can see from the map.

Are payday loans legal in the United States?

At the federal level, yes and payday lenders are subject to regulation by the Consumer Financial Protection Bureau as well as the Federal Trade Commission along with the Truth in Lending Act that requires them to disclose their finance charges. And there are special protections for military servicemen through the Military Lending Act. However legislation regarding payday loans varies widely between different states. As of 2017, payday lending is legal in 27 states, legal with restrictions in 9, and banned in 14 including my home state of Pennsylvania.

How did payday loans come to be?

The history of payday loans can be dated as far as the early 1900s with some small lenders participating in salary purchases, buying a worker’s salary at less than its value days before the scheduled payday in order to avoid usury laws. Loan sharks and the mafia also had their own payday loan schemes starting from the 1920s. In the 1930s, check cashers cashed post-dated checks for a daily fee until the check was negotiated at a later date and began offering payday loan services in the early 1990s. When banking deregulation caused small community banks to go out of business in the late 1980s which, the payday loan industry sprang up in order to fill the void in the microcredit supply at expensive rates. From there, the industry grew from less than 500 storefronts to over 22,000 and a total size of $46 billion. The number has grown even higher over the years that by 2008, payday loan stores nationwide outnumbered Starbucks shops and McDonald’s restaurants. There are also major banks that offer payday loans as well as companies that offer them online. Deregulation also caused states to roll back usury caps and allow lenders to restructure their loans to avoid them after federal laws were changed.

What do I need to qualify for a payday loan?

According to the CFPB, payday lenders generally require you to have an active checking account, provide proof of income from a job or another source, show valid identification, and be at least 18 years old. Some may have additional criteria like minimum time at your current job or a minimum income to qualify for a certain amount.

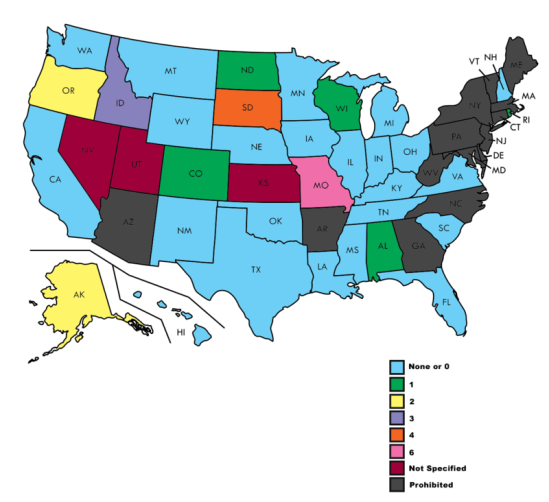

Like payday loans themselves, rollovers and renewals on payday loans also have varying legality among the states. However, they’re usually more or less regulated except in Kansas, Utah, and Nevada.

What does it mean to renew or rollover a payday loan?

According to the CFPB, “Generally, renewing or rolling over a payday loan means you pay a fee to delay paying back the loan. This fee does not reduce the amount you owe. If you roll over the loan multiple times, it’s possible to pay several hundred dollars in fees and still owe the amount you borrowed. For example, if you roll over a $300 loan with a $45 fee three times before fully repaying the loan, you will pay four $45 fees, or $180, and you will still owe the $300. So, in that example, you would pay back a total of $480.” Some payday lenders give borrowers this option if they can’t afford to make the payment when it’s due. Nevertheless, this practice is legal in only 14 states and most of them place limits on this save Nevada, Utah, and Kansas.

Despite what ads may tell you, most payday loan users are low income workers who usually take them out for recurring expenses over the course of months. This is partly why a lot of users have trouble paying them off.

Who uses payday loans?

According to a Pew study, “Most payday loan borrowers [in the United States] are white, female, and are 25 to 44 years old. However, after controlling for other characteristics, there are five groups that have higher odds of having used a payday loan: those without a four-year college degree; home renters; African Americans; those earning below $40,000 annually; and those who are separated or divorced.” Recent immigrants, Hispanics, and single parents also were more likely to use payday loans. And most borrowers use payday loans to cover ordinary living expenses over the course of months, not unexpected emergencies over the course of weeks (contrary to what the industry states in its ads). So it’s not unusual for borrowers to use more than one. The average borrower is indebted about 5 months a year. In 2013, 12 million people took out payday loans each year.

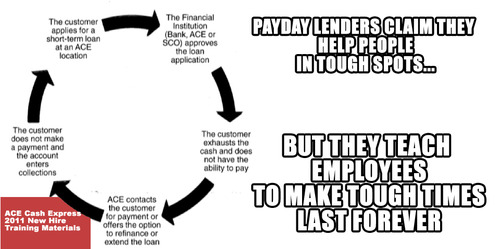

Payday lenders may claim to help people in tight spots. But they ensure employees to make tough times last forever thanks to obscenely high interest rates that may be impossible for some to pay off.

So why do payday loans have a shady reputation?

Payday lenders are notorious for their predatory lending practices of exorbitant higher fees and interest rates than traditional loans that don’t encourage savings or asset accumulation. According to the CFPB, “The cost of the loan (finance charge) may range from $10 to $30 for every $100 borrowed. A typical two-week payday loan with a $15 per $100 fee equates to an annual percentage rate (APR) of almost 400%. By comparison, APRs on credit cards can range from about 12 percent to 30 percent.” If that loan’s not paid on time, then the total cost will be much larger than expected $404.56 within 20 weeks or $2,862.22 within 48. The Pew study states that the average payday loan borrower took out 8 loans of $375 each and paid interest of $520 across the loans within a year.

Payday loans are usually marketed towards low-income households because they often can’t provide collateral in order to obtain a low interest loan or lack access to a traditional bank deposit account. Families who use payday loans are disproportionately black or Hispanic, recent immigrants, and/or under-educated since these individuals are least able to secure normal lower-interest-rate forms of credit. The payday loan industry takes advantage of the fact that most of their borrowers don’t know how to calculate their loan’s APR and don’t realize they’re being charged rates up to 390% interest annually. Those higher interest rates are likely to send borrowers into a debt spiral where they must constantly renew. And according to the Center for Responsible Lending, almost of half of payday loan borrowers will default within the first two years. Taking out payday loans also increases the possibility of economic difficulties that make it hard to pay the rent, mortgage, and utility bills. Such difficulties can also lead to homelessness as well as delays in medical and dental care along with the ability to purchase drugs. Since payday lending operations charge higher interest-rates than traditional banks, they have the effect of depleting assets in low-income communities. A consumer advocacy group called the Insight Center reported that payday lending cost the US $774 million a year in 2013.

Payday lenders have also made effective use of the sovereign status of Native American reservations, often forming partnerships with members of a tribe to offer loans over the internet which evade state law. While some tribal lenders are operated by Native Americans, there’s also evidence many are simply a creation of so-called “rent-a-tribe” schemes where a non-Native company sets up operations on tribal lands. The FTC also monitors these lenders as well. And the fact the Military Lending Act imposes a 36% rate cap on tax refund loans and certain payday and auto title loans made to active duty armed forces and their covered dependents as well as prohibits certain terms in such loans illustrates that the payday loan industry has targeted military servicemen.

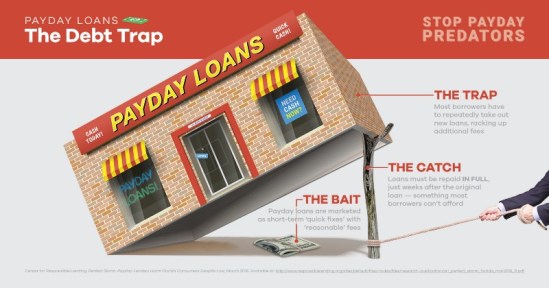

Payday loans are often a debt trap since they target people who can least afford to pay them back. And such debt may lead borrowers to take in more payday loans ensuring a vicious cycle to continue.

How are payday loans a debt trap?

A debt trapped is defined as “a situation in which a debt is difficult or impossible to repay, typically because high interest payments prevent repayment of the principal.” According to the Center for Responsible Lending, 76% of the total volume of payday loans are due to loan churning, where loans are taken out within two weeks of a previous loan. The center states that the devotion of 25-50% of the borrower’s paychecks leaves most borrowers with inadequate funds, compelling them to take new payday loans immediately. And they will continue to pay high percentages to float the loan across longer time periods, effectively placing them in a financial hole.

How do payday loans affect the economy?

Payday loans actually hurt the economy. Though they’re designed to provide consumers with emergency liquidity (despite being normally used to meet normal recurring obligations), payday loans divert money away from consumer spending and towards paying interest rates which can range from 200-500%. In 2011, payday loans cost the US $774 million in consumer spending, $169 million in 56,230 bankruptcies, and 14,000 jobs. States that have outlawed payday lending have lower rates of bankruptcy, a smaller volume of complaints regarding collection tactics, and the development of new lending services from banks to credit unions.

How long does it take to pay off a payday loan?

Borrowers typically have payday loan debt for much longer than the loan’s advertised two-week period, averaging about 200 days. Though most borrowers do know when they’ll pay them off and about 60% of them pay off their loans within two weeks of the days they predict.

Payday lenders can be quite ruthless when it comes to collecting the debts. On some occasions, payday lenders have threatened borrowers with legal action that has led to a small percentage serving jail time.

How do payday lenders collect on loans?

Under federal law, a payday lender can use only the same industry standard collection practices used to collect other debts specifically standards listed under the Fair Debt Collection Practices Act (FDCPA). The FDCPA forbids debt collectors from using abusive, unfair, and deceptive practices to collect from debtors. Such practices include calling before 8 o’clock in the morning or after 9 o’clock at night, or calling debtors at work. In many cases, borrowers write a post-dated check to the lender and if they don’t have enough money in their account by the check’s date, it will bounce. When that happens, payday lenders will usually attempt to collect on the consumer’s obligation first by simply requesting payment. If internal collection fails, some payday lenders may outsource the debt collection or sell that debt to a third party. Yet, a small percentage of payday lenders have in the past threatened delinquent borrowers with criminal prosecution for check fraud which is illegal in many jurisdictions. But over a third of states in 2011 allowed late borrowers to be jailed despite the fact that debtor’s prisons have been federally outlawed since 1833.

Then there’s the matter with Texas, which prohibits payday lenders from suing a borrower for theft if the check is post-dated. But lenders get their customers to write checks for the day the loan is given knowing that they’d bounce since the borrowers didn’t have any money. If the borrower fails to pay on the due date, the lender sues them for writing a hot check. Sometimes they can file criminal complaints. This has led Texas courts and prosecutors becoming de facto collections agencies that warn borrowers they could face arrest, criminal charges, jail time, and fines. On top of debts owed, district attorneys charge additional fees. Borrowers have been jailed for owing as little as $200 and most of them who failed to pay had lost their jobs or had their hours reduced at work.

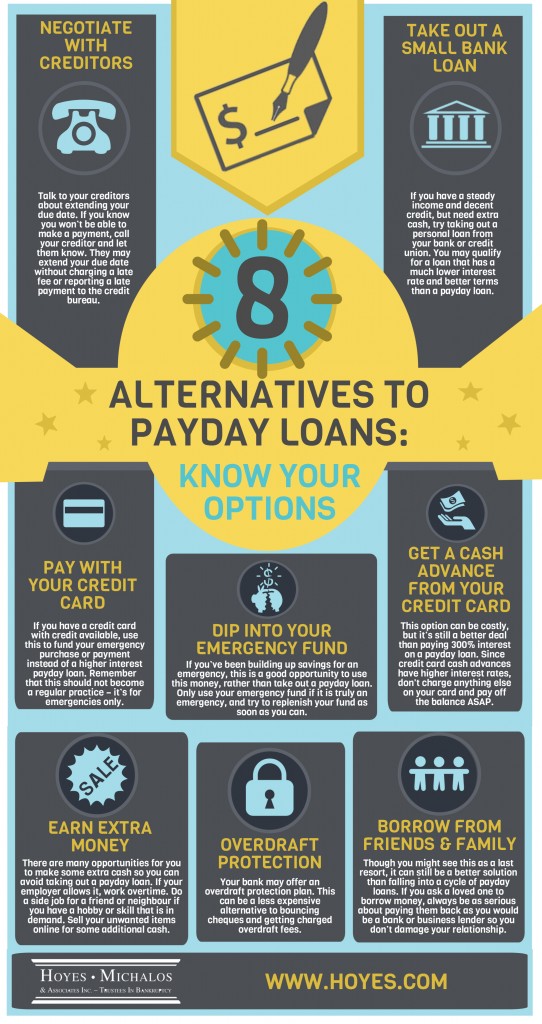

There are several alternatives to payday loans whether it means borrowing money from work or from friends or taking money from a credit union. However, if you need some fast cash before your next payday, it’s better to pay a late fee on your bills than take a payday loan. Because payday loans are nothing but high interest debt traps.

Are there any alternatives to payday lending?

Yes, there are. Credit union loans have lower interest but more stringent terms that take longer to gain approval, employee access to earned but unpaid wages, pawnbrokers, credit payment plans, paycheck cash advances from employers (“advance on salary”), auto pawn loans, bank overdraft protection, cash advances from credit cards, emergency community assistance plans, small consumer loans, installment loans and direct loans from family or friends. Those who own a car can go with an auto title loan which uses the equity of the vehicle as the credit instead of payment history and employment history. You can also take advantage overdraft protection at your bank, establish a line of credit from an FDIC-approved lender. However, if you should consider taking payday loans, always consider the alternatives or at least try to avoid taking them. So if you need to pay your bills before payday, a late fee might be cheaper than a payday loan finance charge.

Yes, payday loans work like that. So remember, if you’re a low income worker in need of money, don’t be embarrassed to ask for help from a friend or employer. Chances are they’d probably not put you through financial hell like the predatory payday loan business. I mean such