For the United States in 2017, the economy is growing, unemployment is low, and consumer confidence is at a decade-long high. Though this would normally create a retail boom, more chains are filing for bankruptcy and rated distressed than at the height of the Great Recession. Cities across the country are facing 6,800 store closings which has become known as the retail apocalypse. This year 19 retail companies have declared bankruptcy including Radio Shack, The Limited, Payless, and Toys “R” Us. Naturally people like to point at Amazon but e-commerce sales in the second quarter only hit 8.9% of sales. So it’s not like these stores are necessarily hurting for business despite declining sales. Besides, most of the retailers already have online stores.

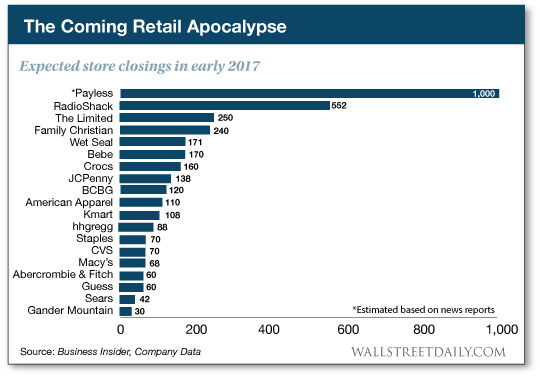

Here’s a chart on the stores closing due to the retail apocalypse. Though we often blame Amazon for this and declining sales, the real cause for this is far more insidious than you can even imagine.

However, the real reason why so many companies are sick has little to do with technological disruption. Rather with debt and a predatory financial scheme. Over the past decade, private equity firms bought numerous chain stores and loaded them up with unsustainable debt payments as part of their business strategy. Billions of dollars of this debt comes due within the next few years. As Bloomberg wrote in a recent article, “If today is considered a retail apocalypse, then what’s coming next could truly be scary.” The retail sector has already lost hundred thousand jobs from October 2016 to April 2017. In the following June, 1,000 stores closed within a week. And it will only get worse. This year only $100 million in retail debt came due this year. But there will be $1.9 billion next year and $5 billion on average due between 2019-2025. This threatens retail sales and cashiers who make up 6% of the entire US workforce and a total of 8 million jobs. And since these workers aren’t confined to any one region, the entire country will share their pain. In the Pittsburgh area where I live, 26.8% of retail loans are delinquent. States like Michigan, Illinois, West Virginia, and Ohio are among the hardest hit where retail employment has declined over the last decade and those will likely spread. Meanwhile, any states like Florida, Arkansas, and Nevada have overly relied on retail for job growth and will feel more pain as the fallout deepens. States like Alabama, Louisiana, New Hampshire, Mississippi, and South Carolina have the highest concentration of cashiers. As the debt comes due, expect more displaced low-income workers, shrinking local tax bases, and investor losses on stocks, bonds, and real estate.

The tragedy of Sears is a major example of how private equity can be so insidious. Once a retail bastion, it’s now facing bankruptcy thanks to overbearing debt and mismanagement by hedge fund manager Eddie Lampert.

The most famous example of this is Sears which is now closing hundreds of stores and facing bankruptcy. Once a bastion in America’s consumer-based economy, it has been run to the ground by none other than hedge-fund king Eddie Lampert. A former Yale roommate of Treasury Secretary Steve Mnuchin, arranged the Sears-Kmart merger and immediately started shifting revenue to shareholders. In addition, he spent $6 billion on stock buybacks to reward investors and raise the share price. More importantly, Lampert personally lent billions to Sears Kmart which increased its corporate debt. As its in-store sales lagged, Sears sold off major assets like its Craftsman brand tools and Land’s End outdoor equipment to pay for the loans. He also split ownership of 266 Sears and Kmart buildings into a real estate investment firm called Seritage. Last year, Sears and Kmart stores paid $200 million in rent on these properties they once owned which ate up its operating revenue. Even as Sears’ very existence is in question, Lampert will likely come out ahead. He’s enjoyed fees from all the lending to Sears and he’ll recoup more money in any restructuring even if Sears has to sell off inventory to do it. As Seritage’s shareholder, Lambert’s hedge funds can profit from higher rents charged to new retail outlets moving into shuttered Sears and Kmart locations. In fact just this year, a Kmart near where I lived and used to shop closed down and I knew some people who worked there.

This is a Kmart store in Rostraver Township, Pennsylvania that’s near where I live. On June 7, 2017, it was announced this store was closing. I’ve shopped at this place on many occasions and knew some of the people who worked there. Kind of a shame. I’ve also heard that the Kmart in Mount Pleasant Township closed earlier this year as well. Kind of a shame.

Sears’s mismanagement reflects an ongoing pattern of private equity takeover artists benefitting from crippling the companies they purchase. Golden Gate Capital and Blum Capital, the 2 firms behind Payless, paid them $700 million in dividends in 2012 and 2013 on the company’s back. Payless filed for bankruptcy this year and closed 400 stores. Toys “R” Us filed for bankruptcy in September unable to sustain between $400-$500 million in annual interest payments on $5.2 billion long-term debt. Private equity firms, including Bain Capital and longtime firm Kohlberg Kravis Roberts, stripped out nearly $2 billion in cash as debt levels rose. And Toy “R” Us’s profitability was increasing when it filed for Chapter 11 since sales in the toy sector had been rising annually by 5% over the past 5 years.

Toys “R” Us wasn’t among the worst casualties in the retail apocalypse. But its filing for bankruptcy in September came as a shock because its profitability had increased and its business was mostly stable. However, the real reason was that the toy store chain was overburdened with debt to private equity firms that bought it out in 2005.

What you see is a robbery in progress. Private equity firms borrow massively to buy companies and use corporate cash reserves to pay themselves back. Workers contributing the value to the business see nothing but the possible job cut since companies usually cut staff to service the debt. When the company collapses under the borrowing weight, all workers lose their jobs even when sales are up. Though troubled retailers have billions of borrowings on their balanced sheets like Sears, sustaining that load will only become more difficult even for healthy chains like Toys “R” Us. Private equity firms defend that their business model returns companies to fiscal health thanks to superior management. But this isn’t what we see in the retail apocalypse. Retail firms typically roll over debt to buy time and avoid bankruptcy. However, interest rates have increased since the last set of buyouts several years ago, making that prospect more expensive. Now these overleveraged companies are finding it difficult for anyone to agree to refinance. As a result, delinquent payments on shopping centers and other commercial real estate have spiked as high as one quarter of all loans in some parts of the country.

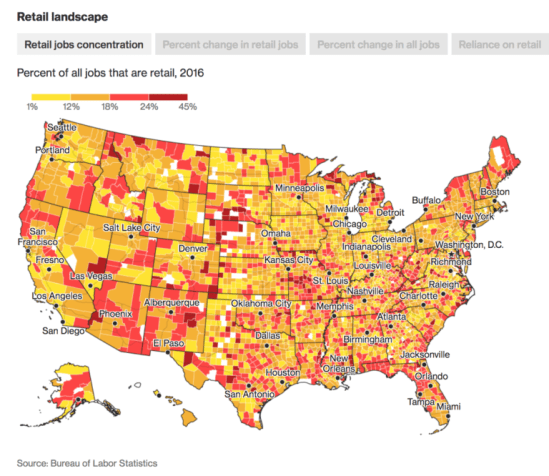

This is a map from Bloomberg showing the concentration of retail jobs all over the country from 2016. Due to private equity overleveraging, the retail apocalypse will only get worse as debts come due. This could mean millions of Americans losing their jobs.

Yet, private equity firms don’t receive a lot of attention which is why I devised this handy FAQ for you to look at. If there is a reason we should care about private equity firms, is that they play a huge role in our economy. Though not all PE firms aren’t predatory finance schemes, many are. And the fact they’re less regulated than banks only exacerbates matters when these vulture capitalists put a company under. Predatory financial schemes hurt everyone. They kill jobs and businesses as well as ruin communities and whole economies. As of 2012, private equity firms own companies employing about 1 out of 10 Americans. This makes them hugely important since they’re basically America’s biggest employers. If you work for a PE-owned company, you might stand a chance of losing your job within the next few years. Now I’m not a fan of corporate America and have the criticized the retail industry for mistreating their workers on shit wages, unpredictable schedules, and anti-union activities. But I understand the retail industry does play a key role in the US economy. Even a shit job like cashier is a job nonetheless. And people rely on these jobs to support their families. Thus, I believe we need to understand what these private equity firms do and how many of them can be a business’s best friend or its worst nightmare. So here is a handy FAQ for reference. Besides, since millions of Americans will lose their jobs over private equity activities, they should know the truth as to why.

What is a private equity firm?

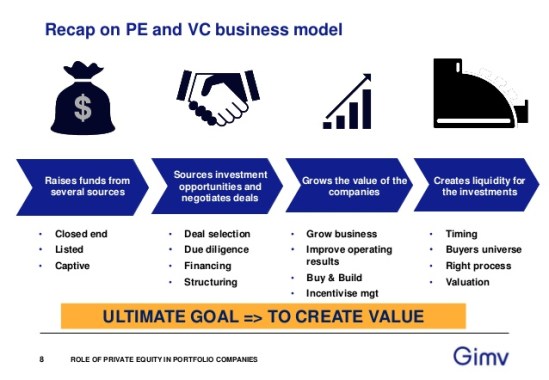

This is a diagram of a private equity firm business model. Though I suppose more of an advertisement since it seems to create a positive image.

A private equity firm is an investment management company that provides financial backing and makes investments in the private equity of startup or operating companies through an array of loosely affiliated investment strategies. Usually described as a financial sponsor, each firm takes a bunch of money for a private equity fund and buys up these companies. They do this by usually matching rich people and institutions with more money than they know what to do with to middle market companies who need access to a steady flow of cash. First, the equity firm buys the company through an auction. Second, the firm then increases the company’s value whether through upgrading its accounting system, a procurement process and information technology, or laying off workers and closing unprofitable operations. In return, the private equity firm will receive a periodic management fee and a 20% share in the profits earned. With their investors, private equity firms will acquire a controlling or substantial minority position in a company and then look to maximize that investment’s value. And they generally receive a return on their investment through one or more of the following (if they’re lucky):

Initial Public Offering (IPO)- company’s shares are offered to the public, typically providing a partial immediate realization to the financial sponsor and public market into which it can later sell additional shares. Through his process, a privately held company transforms into a public one. IPOs are usually used by companies to raise the expansion of capital, possibly to monetize investments of early private investors, and become publicly traded enterprises. Companies selling shares are never required to repay its capital to public investors who pass money between each other afterwards. Although an IPO offers many advantages, there also significant disadvantages such as the costs usually associated with the process and the requirement to disclose information that could provide helpful information to competitors. Details of the proposed offering are disclosed to potential purchasers in the form of a lengthy document known as a prospectus. Most companies undertake an IPO with assistance from an investment firm acting in the capacity of an underwriter. Since underwriters provide several services like help with correctly assessing share value and establishing a public market for shares.

Merger and Acquisition (M&A)- one company is sold for either cash or shares in another. As an aspect of strategic management, M&A can allow enterprises to grow, shrink, and change the nature of their business or competitive position. From a legal perspective, a merger is a legal consolidation of 2 entities into one. Whereas, an acquisition occurs when one entity takes ownership of another entity’s stock, equity interests, or assets. From a commercial and economic point of view, both types of transactions generally result in consolidation of assets and liabilities under one entity and the distinction is less clear. A transaction legally structured as an acquisition may lead to placing one party’s business under the other party’s shareholders’ indirect ownership. At the same time, a transaction legally structured as a merger may give each party’s shareholders partial ownership and control of the combined enterprise. This deal may be euphemistically called a “merger of equals” if both CEOs agree that joining together is in the best interest of both of their companies. Meanwhile, when the deal is unfriendly (like when a target company’s management opposes the deal), it might simply be seen as an “acquisition.”

Recapitalization- cash is distributed to the shareholders (in this case the financial sponsor) and its private equity funds from a company’s cash flow or raising debt or other securities to fund the transaction. As a type of corporate reorganization involving substantial change in a company’s capital structure which may be motivated for a number of reasons. Usually, the large part of equity is replaced with debt. In more complicated transactions, mezzanine financing and other hybrid securities are involved.

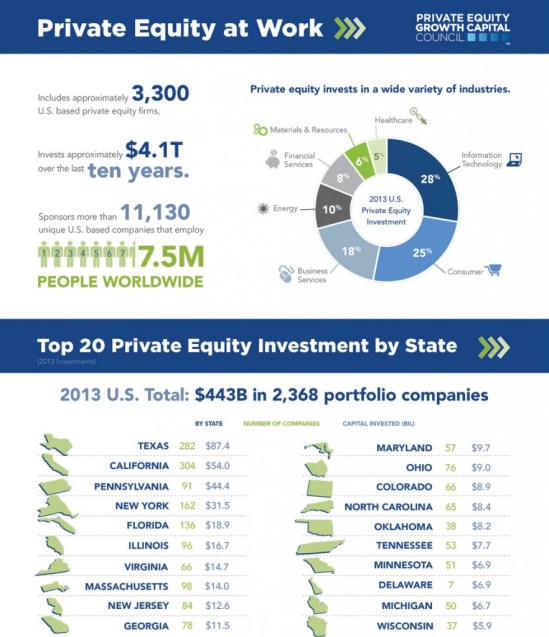

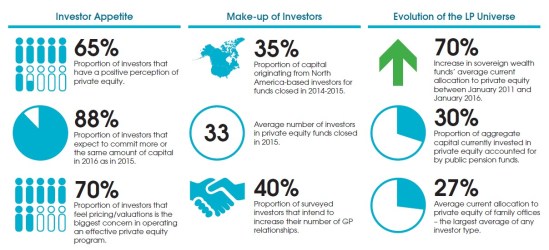

As you can see from this infographic, private equity is widespread. As you can see, they’re a major presence in the US economy. Of course, the industries they invest most into are consumer and information technology, which should surprise anyone.

But we should understand that often the effort to fix up the company fails and bankruptcy is the outcome. So while the rewards are great so are the risks. Back in 2012, The Wall Street Journal did an analysis of the 77 businesses Bain Capital invested during former Governor Mitt Romney’s tenure. It found that 22% either filed for bankruptcy or shut down within 8 years of Bain’s investment. Even several companies that initially provided Bain with huge profits later ran into trouble. Of the 10 deals producing more than 70% of Bain’s gains, 4 eventually filed for bankruptcy. But the companies that succeeded were hugely profitable as the Journal concluded that Bain turned $1.1 billion into $2.5 billion in gains in the 77 deals.

So they’re like hedge funds?

Not exactly. Private equity firms characteristically make longer-hold investments in target industry sectors or specific investment areas where they know a lot about. They also take on operational roles to manage risk and achieve growth through long-term investments. Private equity firms and investment funds shouldn’t be mistaken for hedge fund firms which typically make shorter-term investments in securities and other more liquid assets within an industry sector but with less direct influence and control over a specific company’s operations. And hedge fund firms usually bet on both the up and down sides of a business or an industry sector’s financial health.

What is a private equity fund?

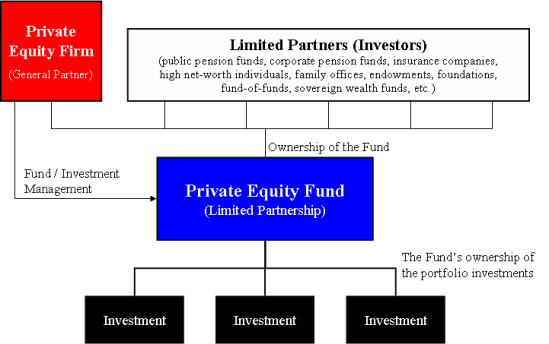

This is a diagram of a generic private equity fund. The private equity firm acts as the general partner while the limited partner investors usually supply the cash for the investments.

Private equity funds usually have a general partner (GP) raising capital from cash-rich institutional investors like pension plans, universities, insurance companies, foundations, endowments, and high-net-worth individuals investing as limited partners (LPs) in the fund. Before buying the company, the GP (who makes all the fund’s decisions), devises a plan for how much debt to use, how the company’s cash flow will be used to service the debt, and how the PE firm will exit at a profit. The private equity firm typically has very little of its own money at risk, only investing 2% or less in the fund while the LPs put up 98% of the equity. But it claims 20% of any gains from these companies’ subsequent sale. Among the terms set forth in the limited partnership are the following:

Though I’ve already shown a private equity fund’s basic structure, here’s a more detailed chart. You can see the kinds of partners who invest as well as the strategies used.

Term of the Partnership- usually a fixed-life investment vehicle that’s 10 years plus some number of extensions.

Management Fees- annual payments made by investors in the fund to its manager to pay for the private equity firm’s investment operations (usually 1% or 2% of the committed capital to the fund).

Distribution Waterfall- the process in which the returned capital will be distributed to the investor and allocated between the Limited and General Partner. This waterfall includes the preferred return, which is the minimum rate of return (e.g. 8%) which must be achieved before the GP can receive any carried interest, which is the profit share paid to the GP above the preferred return (e.g. 20%).

Transfer of an Interest in the Fund- Private equity funds aren’t intended to be transferred or traded. Though they can be transferred to another investor but such transfer must receive the fund manager’s consent and is at the GP’s discretion.

Restrictions on the General Partner- the fund’s manager has significant discretion to make investments and control the fund’s affairs. However, the LPA does have certain restrictions and controls and is often limited in the type, size, or geographic focus of investments permitted, and how long the GP can make new ones.

Can you describe each private equity firm investment strategy?

Certainly. Here are some in depth descriptions of some major strategies. Though they’re not the only kind of ways private equity firms invests.

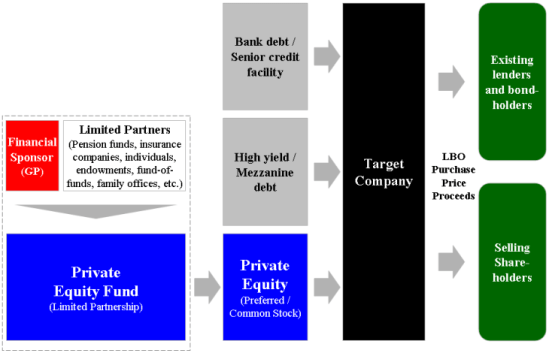

The main investment strategy private equity firms uses is the leverage buyout. This involves buying a company with a combination of equity and debt and using its cash flow as collateral. In fact, it’s usually on the company to pay back the debts. This practice has been prone to plenty of overleveraging and abuse like in the case with Sears.

Leverage Buyout (LBO)- a financial transaction in which a company is purchased with a combination of equity and debt so its cash flow is the collateral used to secure and repay the borrowed money. Since the debt costs less than capital and equity, it serves to reduce the acquisition’s overall financing costs. After all debt costs less than capital and equity because interest payments reduce corporate income tax liability while dividend payments don’t. So the reduced financing costs allows greater gains to accrue to the equity, and as a result, the debt acts as a lever to increase the equity’s returns. Though usually employed when a financial sponsor acquires a company, many corporate transactions are usually funded by bank debt which can also represent an LBO. It could take many forms like management buyout (MBO), management buy-in (MBI), along with secondary and tertiary buyout among others. It can occur in growth situations, restructuring situations, and insolvencies. Though LBOs mostly occur in private companies, they can be employed with public companies, too (in a so-called PtP transaction-Public to Private). As financial sponsors increase their returns by employing a very high leverage (like a high ratio of debt to equity), they’re incentivized to employ as much debt as possible to finance an acquisition. In many cases, this can lead to “over-leveraging” in companies in which they don’t generate enough cash to pay their debt, leading to insolvency or to debt-to-equity swaps in which the equity owners lose control over their business to the lenders. This is the main strategy most private equity firms use and typically finance a buyout of a company with 30% equity and 70% debt. Private equity funds use the acquired company’s assets as collateral and put the burden of repayment on the company itself.

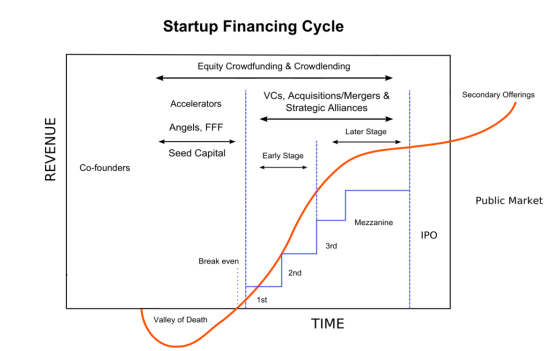

This is a diagram illustrating how start-up companies are typically financed. First, the new firm seeks out “seed capital” and funding from “angel investors” and accelerators. Then if it can survive the “valley of death” (when the start up’s trying to develop on a “shoestring” budget), the firm can seek venture capital financing.

Venture Capital (VC)- a form if financing provided by firms or funds to small, early-stage, emerging funds either seen as highly profitable or potentially so. VCs invest in these early-stage companies in exchange for a return or an ownership stake in those they invest in. They take on the risk of financing risky startups in hopes that some of the firms they support will eventually succeed. The typical VC investment occurs after an initial “seed funding” round also called the Series A Round. A VC will provide this financing in the interest of generating a return through an eventual “exit” event such as the company selling shares to the public for the first time in an IPO or through its merger or acquisition (a.k.a. “trade sale”). In addition to angel investing, equity crowdfunding, and other seed funding options, VC is attractive for new companies with limited operating histories that are too small to raise capital in the public markets and haven’t reached the point where they could secure a bank loan or complete a debt offering. In exchange for the high risk that VCs assume by investing in smaller and early stage companies, they usually get significant control over their decisions along with a portion of their ownership (and consequently value). They also often provide strategic advice to the firm’s executives on its business model and marketing strategies. Additionally, VC is also a way in which the private and public sectors can build an institution that systematically creates business networks for the new firms and industries so they could progress and develop. The VC institution helps identify promising new firms and provide them with finance, technical, expertise, mentoring, marketing “know how,” and business models. Once integrated into the business network, these firms are more likely to succeed as they become “nodes” in the search networks for designing and building products in their domain. However, VC decisions are often biased as well as exhibit an instance of overconfidence and illusion of control like entrepreneurial decisions in general.

Growth Capital- a private equity investment (usually minority investment), in relatively mature companies that are looking for capital to expand or restructure operations, enter new markets, or finance a significant acquisition without a change or control of the business. Companies seeking growth capital will often do so to finance a transformational event in their lifecycle. Unlike VC-funded companies, growth capital companies usually able to make a profit but can’t generate sufficient cash to fund major expansions, acquisitions, or other investments. Because of this lack of scale, these companies generally can find few alternative conduits to secure capital for growth. Thus, access to growth equity can be critical to pursuing necessary facility expansion, sales and marketing initiatives, equipment purchases, and new product development. Growth capital can also be used to affect a restructuring of a company’s balance sheet, particularly to reduce the amount of leverage (or debt). Growth capital is often structured as the preferred equity, though certain investors use various hybrid securities including a contractual return (like interest payments) in addition to an ownership interest in the company. Often, companies seeking that growth capital investments aren’t good candidates to borrow additional debt, either because of the stability of the company’s earnings or existing debt levels.

Mezzanine Financing- any subordinated debt or preferred equity instrument representing a claim on the company’s assets that’s senior only to that of common shares. It can be structured as either debt (usually an unsecured or subordinate note) or preferred stock. It’s often a more expensive financing source for a company than secured or senior debt. The higher cost of capital associated with mezzanine financing is due to it being unsecured, subordinated (or junior) obligation in a company’s capital structure. Should that company default or go bankrupt, mezzanine financing is only paid after all senior obligations are satisfied. Additionally, since it’s usually a private placement, mezzanine financing is often used by smaller companies and may involve greater leverage levels than issues in the high-yield market which involve additional risk. But in compensation for the increased risk, a mezzanine debt holder requires a higher return for their investment than a more senior debt holder.

Distressed Securities- securities over companies or government entities experiencing financial or operational distress, default, or are under bankruptcy. As far as debt securities, this is called distressed debt. Purchasing or holding distressed debt creates significant risk due to the possibility that bankruptcy may render such securities worthless (zero recovery). Deliberate investment in distressed securities as a strategy while potentially lucrative is significantly risky as the security may become worthless. Doing so requires significant levels of resources and expertise to analyze each instrument and assess its position in an insurer’s capital structure along with the likelihood of ultimate recovery. Distressed securities tend to trade at a substantial discounts to their intrinsic or par value and are considered below investment grade. This usually limits the number of potential investors to large institutional investors like hedge funds, private equity firms, and investment banks.

Why would anyone invest in a private equity fund?

Though private equity has earned a reputation as corporate saboteurs outside Wall Street, this kind of investment is quite popular among investors. As you can tell from these stats, the notion of private equity won’t go away soon.

Private equity funds are illiquid and managed by active investors. Those familiar with common index funds such as those of ordinary investors might hold in their investment portfolios might lead you to believe a private equity fund investment is foolish. But private equity funds do have a number of good advantages.

1. Taking companies private is incredibly profitable- When a private equity firm takes a company private from the public market, it has 100% of the ownership and thus can claim all its profits and control all capital allocation. Thus private equity firms have unlimited control over what goes on in the company unlike public equity investors. So they could claim all cash flows in the company.

2. Equity returns in short time frames- It wouldn’t be wise to invest in a portfolio of 100% stock if you’ll need the money within the next 5-7 years. Yet, since private equity firms take companies private, they reap the full ownership benefits (profits) and then resell the companies within 5-7 years in the future. During this time period, private equity investors receive equity-like returns in a time period that would only be safe for fixed-income investments.

3. Leverage- Private equity funds take money from investors and then leverage it with bank loans and bond issues from their newly acquired companies to boost returns for their investors. If a private equity firm takes a company private at 10x earnings of 10% per year, it can do very well for its limited partners by leveraging those earnings with cheap debt. It’s kind of like buying real estate, which when leveraged with bank loans, can be an excellent one.

4. Exits- Private equity funds are designed to exist only for a period of spanning less than a decade. When the fund reaches the end of its designed life, it “exits” its holding by selling them. A common exit is to sell a private equity position to a competing firm or to list private companies on the public markets through an IPO.

Why would a company seek private equity financing?

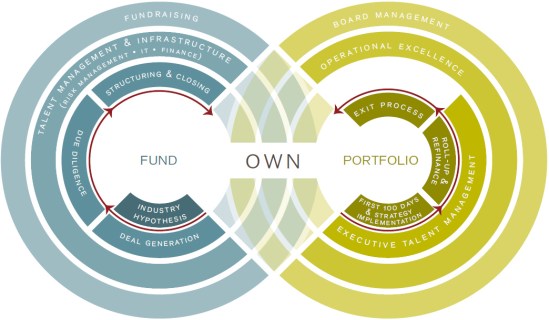

Here’s a cycle of private equity financing from a firm’s site. Though this seems more catered to investors and has a rather positive spin on it.

Private equity financing provides several advantages to companies such as the following.

1. Active involvement- Unlike other funding options, private equity firms are much more hands on and will help a company reevaluate every aspect of their business to see how it can maximize its value. Having experienced professionals in a business can also result in major improvements.

2. Incentives- Private equity firms need a business to succeed since they borrow a lot of money to make their investments and have to pay that back and generate a return for their investors. Individual partners in private equity firms often have their own money invested as well and make additional money from performance fees if they make a profit. So they have strong incentive to increase a company’s value.

3. Large amounts of funding- Private equity can provide larger amounts of money than other options since deals are usually measured in hundreds of millions of dollars. This kind of money can have a massive impact on a company.

4. High Returns- Combinations of major funding, expertise, and incentives can be very powerful on companies. According to a 2012 study by the Boston Consulting Group, more than 2/3 of private equity deals resulted in the company’s annual profits grow by at least 20% while nearly half of the deals generated a profit growth of over 50% a year or more.

5. Patient Investors- Since private equity firms invest in a company to make it more valuable within a number of years before selling to a buyer appreciating the lasting value created, their investors are less concerned with short-term performance targets though they do have their eyes on the prize. Sometimes such firms are also known to offer private equity back office services to other firms or companies needing them for investments.

What are the disadvantages of private equity financing?

At the same time, private equity financing come with an array of disadvantages such as the following.

1. Dilution/Loss of Ownership Stake- Other funding options let the owner still stay in control of the company despite the investment’s costs. A company may receive much more money with private equity, but the owner has to give up a large share of the business. Private equity firms often demand a majority stake and sometimes leave the owner with little or nothing in ownership. It’s a bigger trade and one many business owners balk at.

2. Loss of Management Control- Beyond money, a business owner can lose direct control of their company. The private equity firm would want to be actively involved which can be a good thing. But it can mean losing control of basic elements in the business like setting strategy, hiring and firing employees, and choosing the management team. Since the private equity firm’s stake is usually higher, the loss of control is much greater. This is especially true when it comes to the private equity firm’s “exit strategy” which might involve selling the business outright or other options that don’t form part of the owner’s plans. Then there’s the fact that private equity decision-making has been shown to suffer from cognitive bias such as illusion of control and overconfidence.

3. Different Definitions of Value- Private equity firms exist to invest in companies, make them more valuable, and sell their stakes in large profits. Mostly this can be good for the companies involved since any business owner would want to create more value. But a private equity firm’s definition of value is very specific and limited since it’s focused on a business’s financial value on a particular date about 5 years after the initial investment when the firm sells its stake and books a profit. Business owners, by contrast have a much broader definition of value with a longer-term outlook and more concern for relationships with employees and customers as well as reputation. Such difference can lead to clashes.

4. Eligibility- Private equity firms look for particular types of companies to invest in which have to be large enough to support those major investments and offer potential for large profits in a relatively short time frame. This means that a company must have very strong growth potential or it’s in financial difficulties and is currently undervalued. A business that can’t offer investors a lucrative investment within 5 years will struggle to attract interest from private equity firms.

5. Debt Accumulation- Private equity firms use significant amounts of debt to perform deals in financial markets. This can significantly damage not only the company who has to pay for the debt but also to investors and financial markets as well. Not to mention, they charge their companies a bunch of hidden fees. They also make the companies sell their real estate and pay a higher rent to remain on the property, too.

6. Lack of Transparency- Though oversight on private equity firms has increased since 2008, they’re still less regulated than more traditional forms of financing. Private equity also adheres to some practices that alarm politicians. One tactic is a fee-waiver conversion which intentionally directs a greater amount of an investor’s capital away from higher-taxed fees and into a more favorably taxed category.

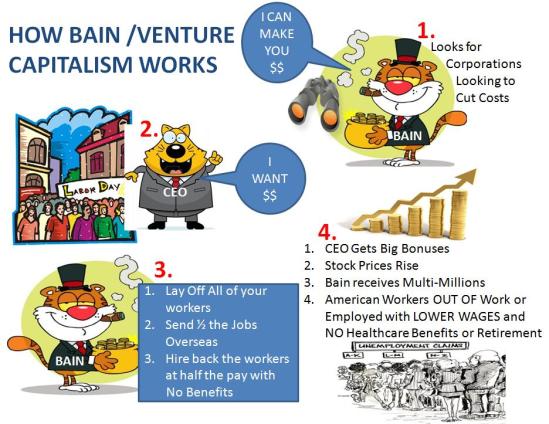

So what’s with the vulture capitalist reputation?

Though not all private equity firms are vulture capitalists, there are plenty of large firms that have acquired such reputation. One of these was Mitt Romney’s Bain Capital as you can see on this cartoon chart.

Private equity firms are notorious for making money for their investors without regard to stakeholders in the business. In most cases, private equity firms acquire the kinds of companies that are already in poor financial health, lack a competitive environment, or have poor managers. They want to acquire companies cheap and that means buying companies they believe have more value than Wall Street is willing to realize. Sometimes this means buying companies everyone knows will go out of business. Sometimes a private equity fund performs as advertised using reasonable amounts of debt and providing access to management and expertise and financial resources. This usually involved smaller companies with few assets that can be mortgaged but many opportunities for operational improvements.

This is Joshua Kosman. In 2009, he wrote a book called The Buyout of America arguing that private equity firms are terrible and will cause the next credit crisis. In his intro he writes, “I believe the record shows that PE firms hurt their businesses competitively, limit their growth, cut jobs without reinvesting the savings, do not even generate good returns for their investors, and are about to cause the Next Great Credit Crisis. Leadership is needed to rally opposition to close the tax loopholes that make this very damaging activity possible.” So far this year’s retail apocalypse is proving him right.

However, the reality is that private equity firms almost always buy larger and profitable companies that already have modern management systems in place as well as substantial assets that can be mortgaged. Here, private equity firms use debt and financial engineering strategies to extract resources from healthy companies. This earns them a reputation for using strategies that critics say play out more as “vulture capitalism”- a phrase that some people use to describe the process where investors make enormous profits while needlessly laying off workers. Private equity investors may increase their investment in companies they own by replacing senior management, reducing the workforce, selling off assets, and essentially gutting the company for profit. A private equity firm could buy a sizeable company, load it up with debt, and then take the money out. After improving their short-term earnings through cuts, it can borrow money and pay itself a dividend. In good times, it can collect a disproportionate share of the investment returns. But this can set up that company for failure and financial vulnerability. If the debt can’t be repaid, the company, its workers, and its creditors bear the costs. Yet, even when a company fails, a private equity firm still makes money. For instance, from 1987-1995, 22% of the money Bain Capital invested in funds raised went to companies that eventually went bankrupt. But Bain made $578 million, comprising of the bulk of these companies’ profits. Under Mitt Romney, 4 of Bain’s 10 biggest investments ended up bankrupt yet the firm still made a killing. Today, it’s no surprise that private equity activity’s often said to focus on short-term profits over a company’s long term health.

But do they improve businesses? According to author Josh Kosman, that may not be so. Out of the 25 biggest buyouts in the 1990s, 52% of those companies ended up bankrupt. Among the 10 biggest, private equity improved only one of the businesses. In 3 cases, the results were mixed while the other 6 companies would’ve been better off had the private equity firm not acquired them. A report from Moody’s back in 2012 showed that in the 40 biggest leveraged buyouts that took place from 2005-2008, these companies saw a revenue increase by 4% while their strategic peers saw profits rise by 14%.

Another criticism is that studying private equity returns is relatively difficult since private equity funds don’t disclose performance data. As these firms invest in private companies, it’s difficult to examine the underlying investments. Comparing private equity to public equity performance is challenging because private equity fund investments are drawn and returned over time as investments are made and subsequently realized. Commentators have argued that a standard methodology is needed to present an accurate picture of performance, to make individual private equity funds comparable and so the asset class as a whole can be matched against public markets and other types of investment. There’s also a claim that private equity firms manipulate data to present themselves as strong performers, making it even more essential to standardize the industry. It’s even worse that private equity firms aren’t as regulated as banks.

Can you describe some shady private equity firm financial engineering practices?

Here’s a chart on the rates in which private equity firms have stripped assets on retailers. Much of this took place in the mid-2010s. Through junk bonds and leveraged loans to fund special dividends to PE owners, retail stores have lost billions in their assets. What a shame.

Certainly. After a buyout, private equity firms often engage in financial engineering that further compromise their portfolio companies. They might have companies take out loans at junk bond rates and use the proceeds to pay themselves and their investors a dividend. They might split a real estate rich company into an operating company and a property company. They then sell off the real estate and repay investors while the operating company must lease back the property and pay the (often inflated) rent. As you can see, this is what Eddie Lampert did to Sears. They may require their companies to pay monitoring fees to the PE firm for unspecified services. Paying these fees reduces the companies’ liquidity cushion and puts them at risk.

What happens to portfolio companies and workers?

Here is a list of companies private equity firm KKR owns. Some of the these brands you might recognized, especially Toys “R” Us which filed for bankruptcy.

In these situations, financial engineering results are predictable. In bad economic times, these companies’ high debt levels (especially in cyclical industries) make them seriously vulnerable to default and bankruptcy. According to one economic study, roughly a quarter of highly leveraged companies defaulted on their debts during the last recession. Though the financial crisis officially ended in 2009, bankruptcies among PE-owned companies continued through 2015. In 2007, a PE consortium acquired Energy Future Holdings which defaulted with $35.8 million in debt in 2014. In 2006, a PE acquired the Las Vegas-based Caesar Entertainment whose long-term debt more than doubled by mid-2007. In 2015, it declared bankruptcy putting over 30,000 union workers at risk. Rigorous econometric studies back these job loss cases. One study found that through 2005, PE-owned establishments had significantly lower employment and wages post buyout than comparable publicly-traded companies. Though PE-owned establishments experienced higher wages and employment growth than their counterparts in their buyout year. But employment rates at PE-owned companies were 3-6.7% lower after 2 years and 6% lower after 5 years.

What happens to the Limited Partner investors?

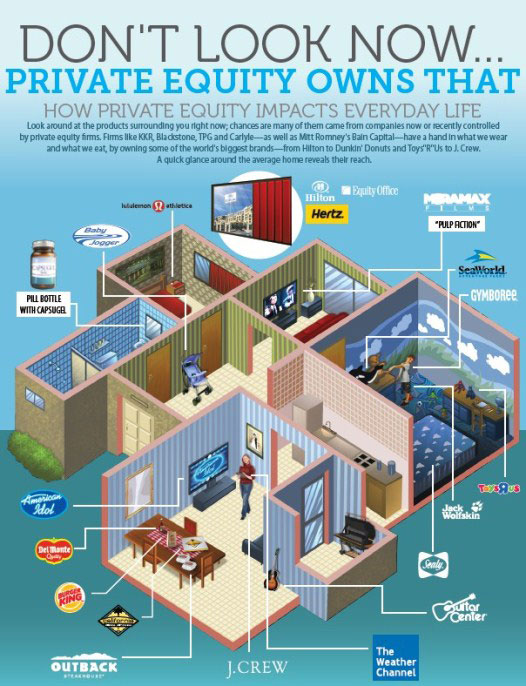

Here’s another chart detailing which companies private equity owns. Many of these will surprise you. But some of them won’t.

Private equity fund performance depends importantly on how investment returns are measured. Private equity firms use the “internal rate of return” (IRR). Finance economists use the “public market equivalent” which compares returns in PE investments from comparable stock market ones. Recent academic studies find that buyout funds don’t deliver outsized returns to investors. Despite industry claims, private equity funds haven’t beaten the stock market since 2006. A recent study indicates a downward trend in PE performance finding that the median PE fund outperformed the S&P 500 by 1.75% in the 1990s and by 1.5% in the 2000s. Private equity returns also need adjustment for PE investments’ greater riskiness. Industry analysts and most investors assume that private equity fund returns should exceed stock market returns by 3%. More than half of US PE funds have failed to meet that standard over the past 25 years. Average PE returns are upwardly skewed by top quartile funds’ outperformance. But recent research shows it’s no longer possible to predicts which funds will outperform the stock market. GPs with top quartile funds have about a 25-cent chance that their next fund will do the same. Same goes for GPs with bottom quartile funds.

What should the US do about private equity firms?

We must hold our politicians responsible for the looming retail apocalypse. After all, our tax code privileges debt by making corporate interest payments tax-deductible. Private equity firms that gut companies and walk away receive tax subsidies to pull it off. This incentivizes them to borrow even more to run the game again. Even more importantly, we need to look at these asset-stripping schemes with more skepticism. The Securities and Exchange Commission can and should police these designed-to-fail corporate bonds resulting from these leveraged buyouts. The SEC should also go after banks underwriting these deals and earning fees off of companies’ misery.

The House Republican tax bill proposed a cap on deductibility on interest payments over 30% of a company’s earnings. The Senate bill defines earnings in such a way to reduce that cap even further. This should discourage some debt-fueled buyouts which private equity firms don’t like. However, the GOP tax plan exempts real estate companies which leaves a gaping loophole. This could help private equity firms that split their business’s operating side from the property side like Sears did. And enable them to put all the borrowing onto the property side and keep deducting the interest. Not to mention, most of the Republican tax bill is a piece of shit that punishes most Americans who don’t own a yacht. So I wouldn’t advocate the Republican tax plan to crack down on private equity anytime soon.

Nevertheless, don’t expect that Donald Trump will do anything about and we shouldn’t be surprised. The Trump administration will likely continue aiding wealthy financiers through regulatory neglect since those people are their donors. Recently, Comptroller of Currency Keith Noreika broke with a years-long crackdown on high-risk corporate lending, signaling that these private equity firms should issue more debt. It’s a shame we don’t have regulators willing to protect workers, investors, and the economy. Because private equity is accelerating a decline that will affect millions in every major city. To do nothing is to let it continue.